“Retirement is when you stop sacrificing today for an imaginary tomorrow.”

Naval Ravikant

Key Takeaways

- Savings targets grow over time, due to inflation increasing the cost of living

- Based on current EPF balances and median salaries, most Malaysians, when they reach the age of 60, will achieve the Basic Savings Level but not necessarily the Adequate Savings Level target

- Increasing the EPF contribution rate or dividend rate over decades can significantly improve outcomes

- Individual Malaysians should think about increasing EPF contributions, building additional retirement funds and increasing salaries to meet long-term retirement targets

Introduction

Welcome to Part 2 of my EPF series! In Part 1, I covered the current situation of EPF balances and targets, highlighting the need to use the right data points and metrics. We established that the goalposts have been shifted, with new Savings Targets that are now for the age of 60 instead of 55.

In this post, I want to look forward to the future. Will the state of Malaysian retirement improve or decline over the next few decades? Which drivers have the most impact to improve EPF balances? Subsequently, based on those drivers, when and under what conditions will Malaysia get out of this retirement crisis?

Let’s dive in.

Defining the question to solve

As a recap from my previous article, we know that EPF has updated its savings targets for a 60-year-old, effective in 2030, as follows:

- RM390k – Basic Savings Level, which covers essential retirement needs. Consider this the bare minimum to survive for at least 20 years post-retirement

- RM660k – Adequate Savings Level, which provides a reasonable standard of living during retirement. Consider this an amount that provides a decent retirement with a margin of safety; and

- RM1.1m, Enhanced Savings Level, supporting greater financial security and independence for a higher quality of life. This would, in theory, provide a comfortable retirement lifestyle (although comfortable is a subjective term)

Leveraging EPF’s own targets, I would think a reasonable way to define success in Malaysia in resolving its retirement funding crisis as

When the median EPF balance for a cohort of EPF members aged 60 exceeds EPF's Adequate Savings target in 2030 of RM660kThat would mean at least half of Malaysians at retirement age have sufficient funds to maintain a reasonable standard of living. No additional government support, or expecting someone else to help support them in their old age.

That would be a great situation to be in, right?

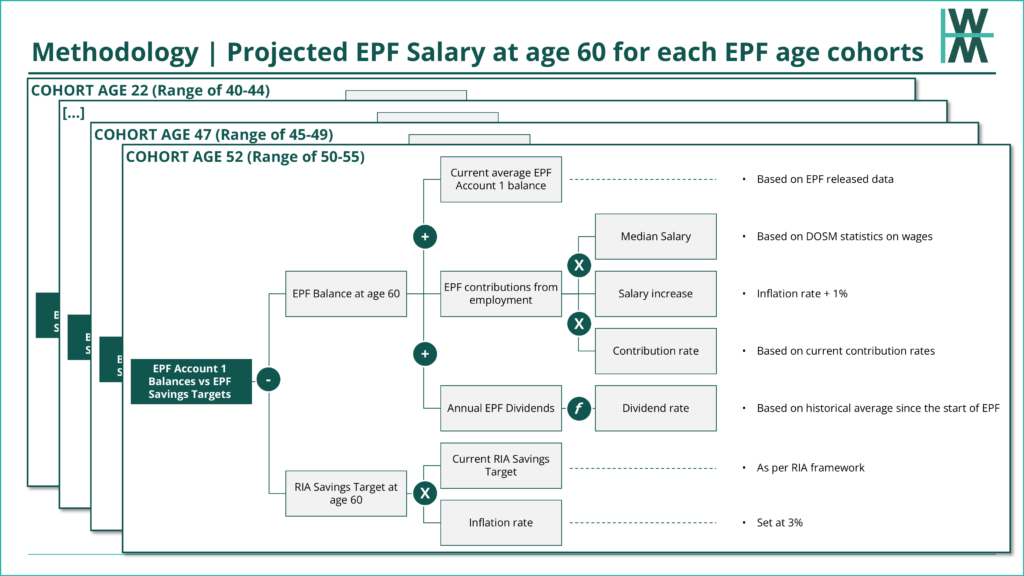

Methodology of EPF Savings Projection Model

Now that we have established a (loosely formed) definition of what resolving the retirement crisis in Malaysia might look like, we can crunch some numbers and forecast when (and also potentially how) this might happen.

The challenge is that for different EPF age cohorts, their retirement age is different, so the Adequate Savings target would be different, likely increasing over time due to inflation (rising costs of living).

So I’ve created a model to project the next few decades for what might happen to EPF balances across the different age cohorts. The methodology is below:

Key assumptions of the model are described below:

- EPF balances: Unfortunately, we only have average balances. EPF, for some unknown reason, only releases median balances for those aged 54. So we’ll have to make do, even if the average balance is skewed upwards due to outliers.

- EPF Accounts: EPF has three accounts. I’m only going to consider the balances in Account 1, and assume that all Account 2 & 3 balances are withdrawn and used up before retirement (maybe this might balance things against the issue of average vs median balance above)

- Age cohorts: EPF divides account holders into 5-year cohorts when publishing statistics. So to project the future, I’m going to take the midpoint age. For example, if the cohort is 50-55, in the model, they will be age 52 (to calculate how many years to retirement)

- EPF rate of return: I’m going to use the historical average ever since inception. That’s 6.2% p.a.

- Inflation rate. This will affect the future targets as the cost of living rises. Whilst current inflation in Jan 2026 is quite low at <2%, I’m going to be conservative and use 3%

- Median salary: Each age cohort is linked to the median inflation for that age cohort in DOSM’s published statistics on wage reports

- Salary increments: Malaysia is still a country with salaries growing at a pretty fast pace. However, let’s keep it conservative, as we don’t know if that ~6%-7% wage growth in Malaysia will last much longer. I’ll stick with 1% above inflation, so 4% p.a.

The maths then gets quite complicated. Essentially, I then forecast, for each cohort, what their EPF balances would be, and then compare that against the inflation-adjusted EPF Savings targets at the time that cohort is 60 years old.

BONUS: Download the EPF projection model

By the way, you can download a copy of the Excel model to play around with the assumptions, or understand how I developed the projections, using the link below

Download the EPF Projection Excel Model hereResults of the EPF projection model

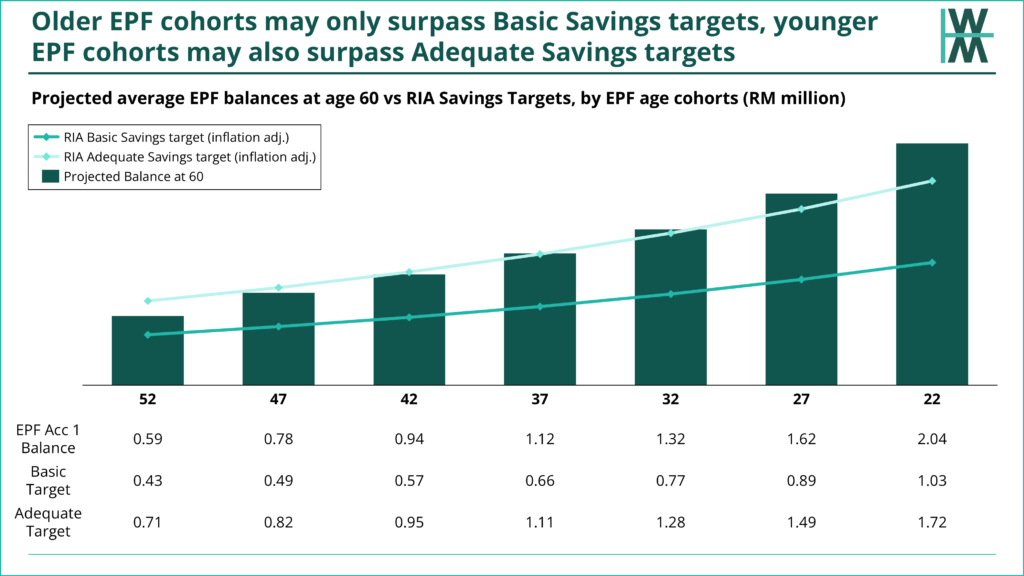

So what do EPF balances look like for each age cohort? Results are below.

Key insights

- All age cohorts, based on average EPF balances, will achieve the Basic level savings target without issue. It’s very achievable as EPF targets are now for age 60 (previously 55), so those extra 5 years matter a lot

- Only cohorts aged 37 and younger will achieve the Adequate Savings target at age 60. That’s at least ~20-25 years away until they reach 60 years old. Older EPF cohorts will be just shy of the Adequate Savings target

- If we estimate median balances for each cohort to be roughly 70% of the average EPF balance (based on current EPF median balances of active accounts aged 54 in EPF’s own annual reports), no cohort will reach a median EPF balance that meets the Adequate Savings level

So does this mean that the average Malaysian will have insufficient funds in EPF to have a reasonable standard of living in retirement, especially those in urban areas?

Perhaps. But models are always wrong. It’s just a question of how wrong it is.

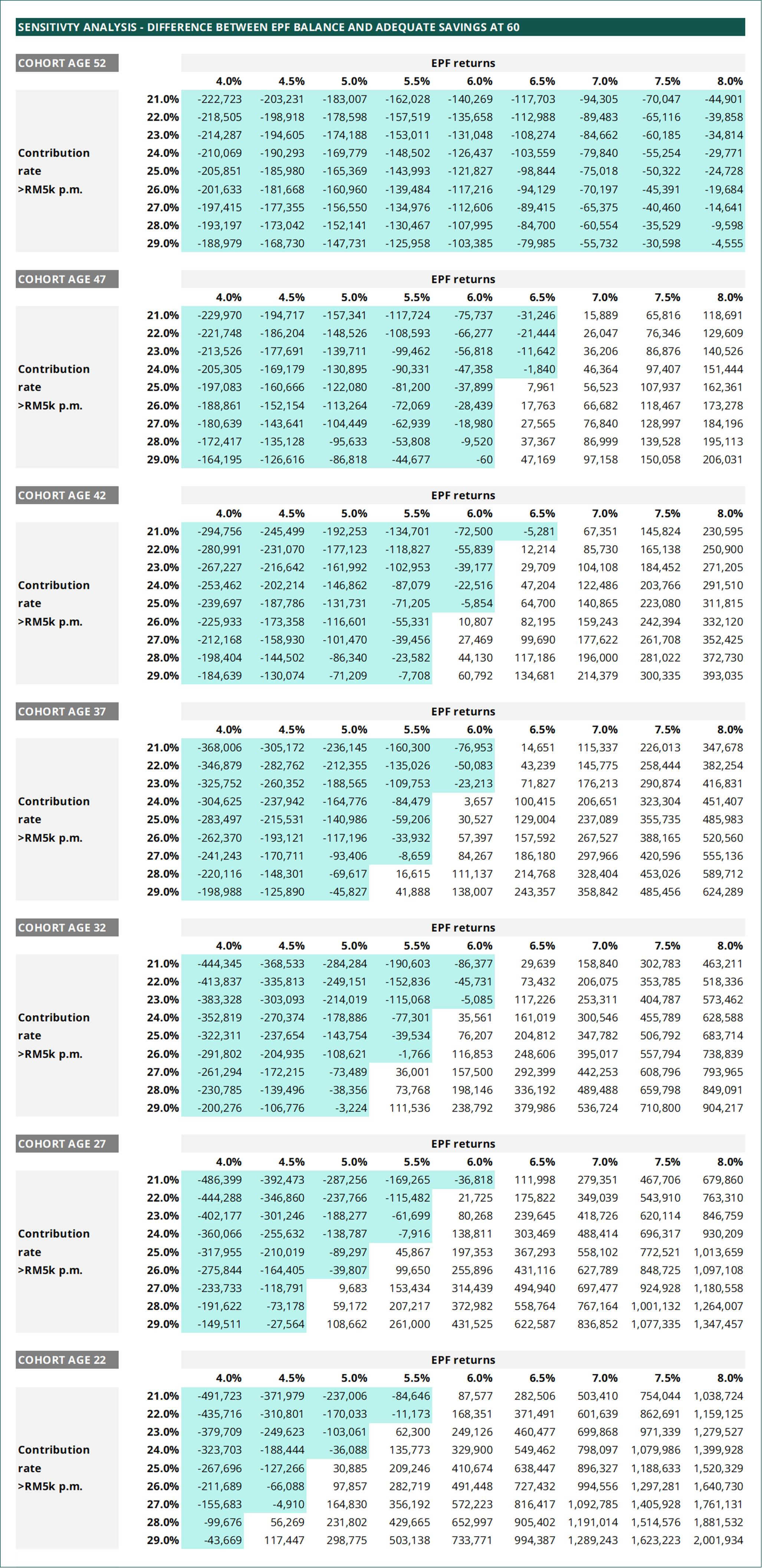

Let’s do a sensitivity analysis to see the results when we analyse a range of numbers for the two biggest drivers of EPF balance growth: (1) the contribution rate and (2) the EPF dividend rate.

Why not analyse changes in salary increments or the inflation rate? Well, partly because they don’t move the numbers as much, but also because those factors are not within direct control of EPF (and to some extent the government), compared to EPF dividend rates and contribution rates, which are driven by investment strategy/execution and contribution rates respectively.

So I’ve listed a few sensitivity tables below, one table for each age cohort. They show for each cohort, the difference between the

- Projected average EPF balance at age 60, and

- Projected Adequate Savings level target

So a positive balance means the average EPF balance exceeds the savings target. A negative number means there is a deficit, which is highlighted in light teal.

Implications for EPF account holders

The takeaways for you

The biggest takeaway is that even small increments or adjustments have really large upsides over the span of decades.

Small adjustments in EPF dividend rates matter a lot over the long term. The more time you have, the more important the amount of compounding is. Even 0.5% matters a lot. We know this based on our mastery of compound interest.

In an ideal world, EPF’s dividend returns could be higher. How about an index fund EPF strategy, Boglehead style, perhaps?. It’s unlikely. Pension and retirement funds must, above all, preserve capital. Market volatility is something which needs to be managed, and EPF does a great job in “absorbing” market fluctuations. EPF does this by not valuing individuals’ EPF balances with underlying investment values, and only paying dividends according to underlying investment income/dividend streams.

Also, increasing the EPF contribution rate by even a few percentage points can significantly improve the long-term outcome for younger-aged cohorts. A 1% increase in the EPF contribution rate results in at least a RM100k difference for someone who is currently around 20-30 years old.

What you can do about it

- Relying solely on EPF in its current state may not be enough. Especially if you live in an urban area with a higher cost of living, e.g. Klang Valley.

- Self-contribute more into EPF, which, as I’ve shown above, with even just a one percentage point more from your salary, can significantly increase your EPF balance at age 60

- Create an additional retirement fund using your own investments. That could be ASB or an index fund. Just make sure it is a simple, boring portfolio that you consistently contribute to. Except for PRS, which I still discourage until there are global index funds available via PRS.

- Earn more. We’re already a nation with struggling wages, so it’s going to be tough. But if you’re someone who actually reads this, you’re likely above average in terms of mindset, skills and experience, and are looking for a higher wealth metagame.

Closing thoughts

One big aspect that’s not spoken about with the retirement deficit is the increasing financialisation of our lives. The longer loan durations and new types of financial/debt products, such as BNPL, mean more and more Malaysians are relying on debt.

And, the duration of the debt is longer. Car loans are 9 years (in other countries, it’s 5). Mortgages are 35 years. Many only purchase a property at the age of 30. That means their mortgage only finishes at 65. What about people who buy a property at 35? Their mortgage will last until they are 70 years old. And many, many Malaysians don’t plan that far ahead and think about if they’ll still be working at 70, or how they can pay off their loan faster, whilst paying for other expenses.

With the lack of both financial literacy and knowledge of how to develop a financial plan, even thinking 10 years into the future is difficult for most Malaysians.

It’s up to Malaysians to take it upon themselves to take retirement planning seriously. We could wait for our institutions to step in and make changes (which is the topic of my next article), but when do you think that will happen?